US: Equities finished narrowly higher but lost momentum late (S&P 500 +0.25% to 6,714; Nasdaq 100 +0.5%; Dow flat) as WTI >$96 stoked inflation concerns. Yields and USD fell ahead of the Fed (expected hold at 3.5–3.75%). Geopolitical escalation remains the dominant macro driver; airlines outperformed, while Boeing flagged production issues and Eli Lilly weakened on valuation concerns.

Europe: Stoxx 600 +0.7%, led by energy (+2.3%, 8th straight gain) on Middle East supply risks. Utilities and insurers +1.6%, banks +0.9% (reassurance on private credit exposure). Strength offset by media (-1.4%) and retail (-0.3%); gains supported by easing rate hike expectations as oil pulled off highs.

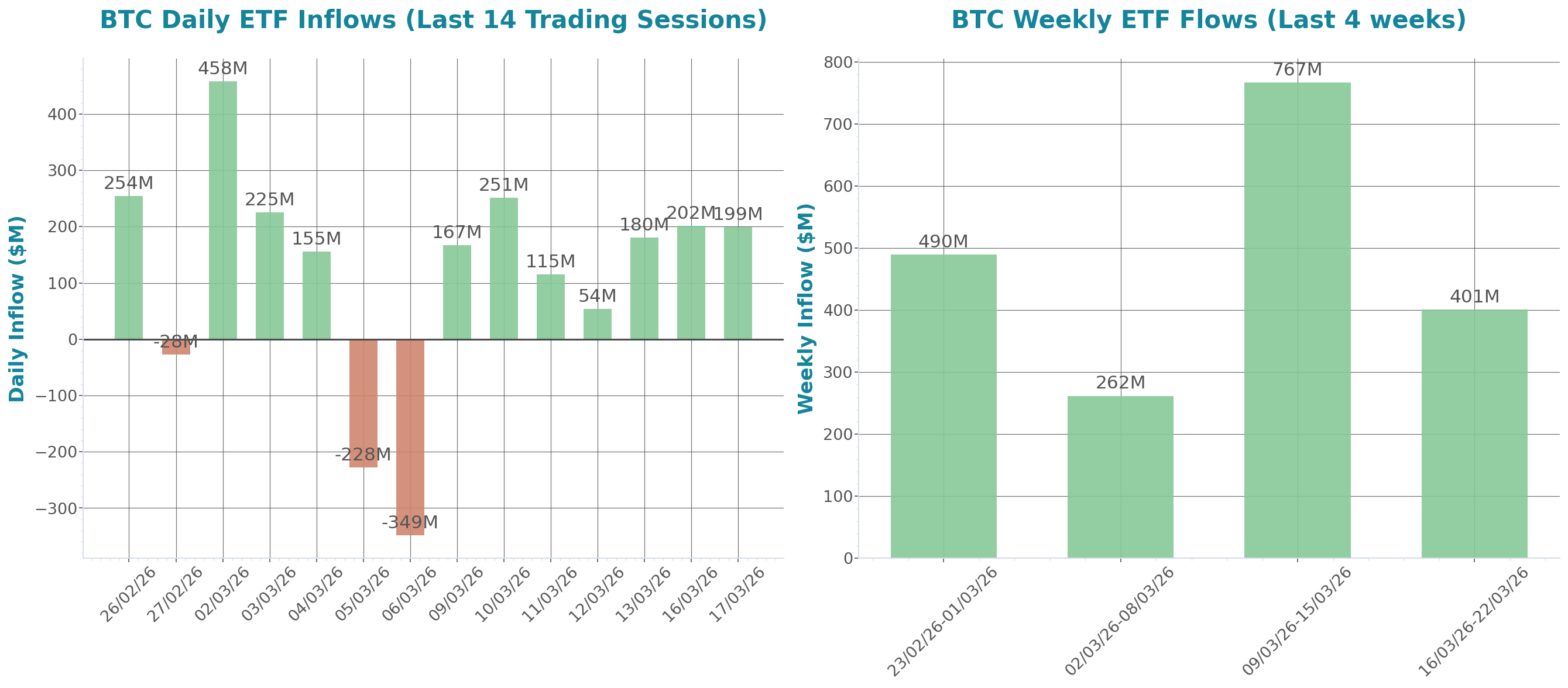

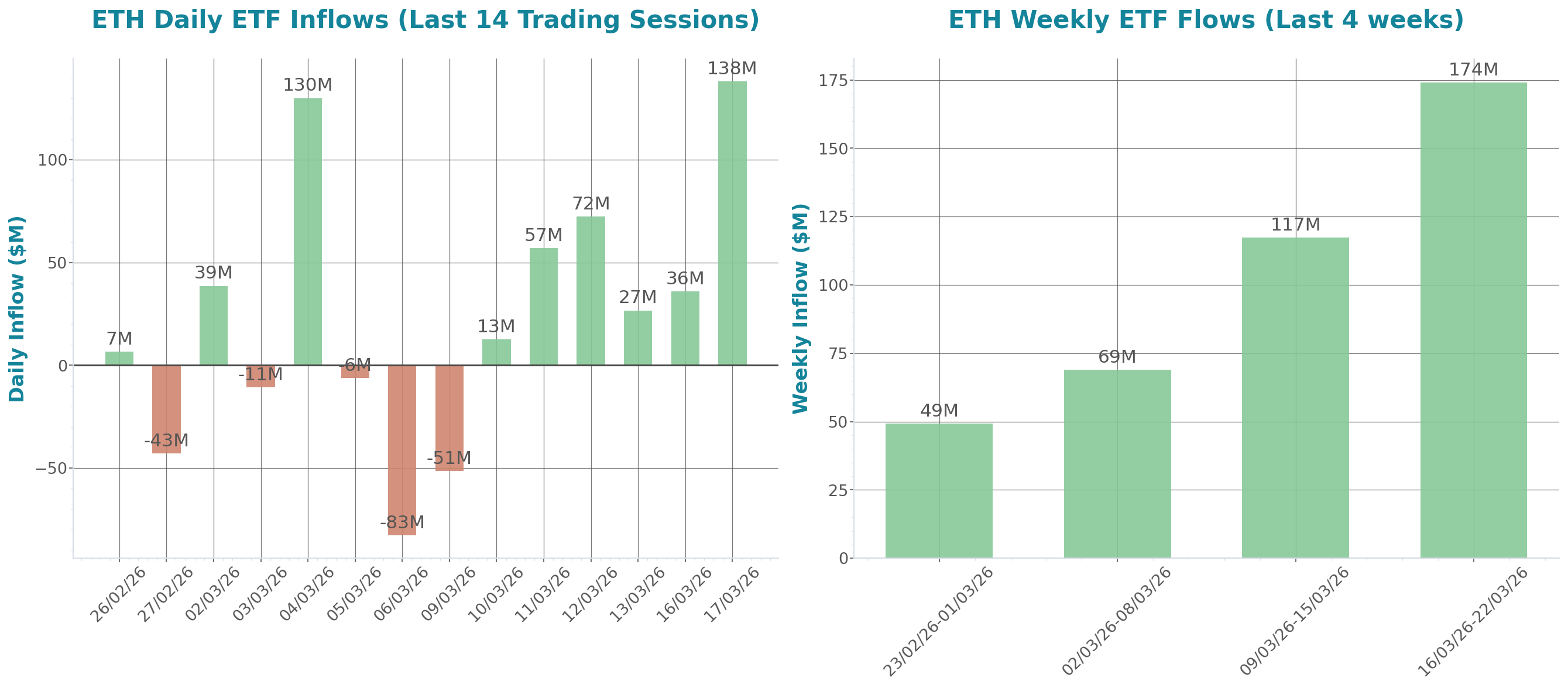

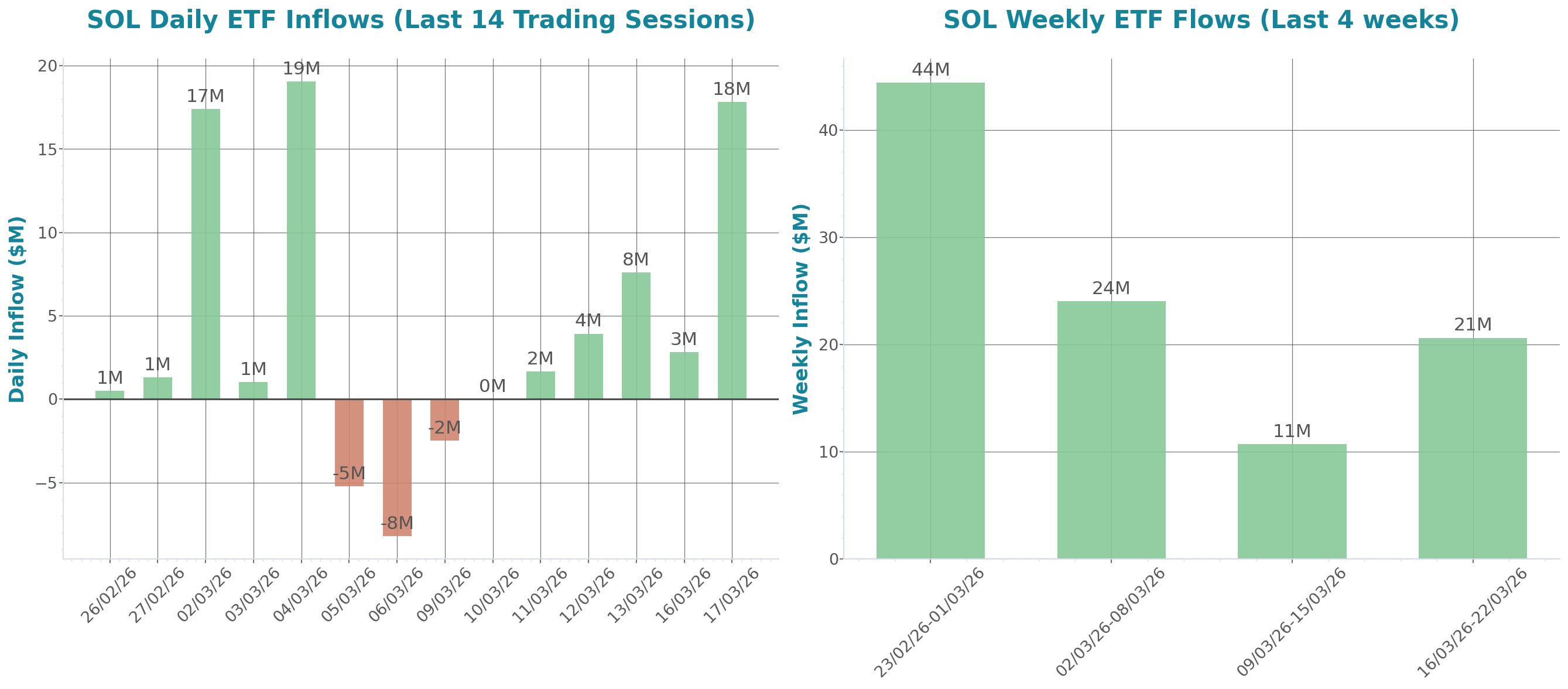

Strategy is buying Bitcoin at a pace massively exceeding new supply—up to ~7× weekly mining output—meaning a single buyer is absorbing more BTC than miners produce, tightening available supply.

Argentina's court orders ENACOM to block Polymarket nationwide due to unauthorized gambling concerns, citing regulatory noncompliance, according to the court's ruling.

Cango reports a $285 million Q4 loss in 2025 as Bitcoin mining costs surge, with shares declining over 84% from $4.50 to $0.68 in six months.

PayPal expands PYUSD stablecoin to 70 countries to reduce cross-border fees and offer rewards on holdings.

Maestro launches Mezzamine, a mining-backed Bitcoin credit market, linking institutional BTC holders with miners seeking capital backed by mining output.

Mastercard agrees to acquire BVNK for up to $1.8 billion to expand its stablecoin and blockchain-based payments services.

XRP reaches a record 7.7 million holders.

Moody's integrates its credit ratings with Canton Network, bringing traditional risk assessment on-chain, in an early step towards blockchain-based financial infrastructure development.

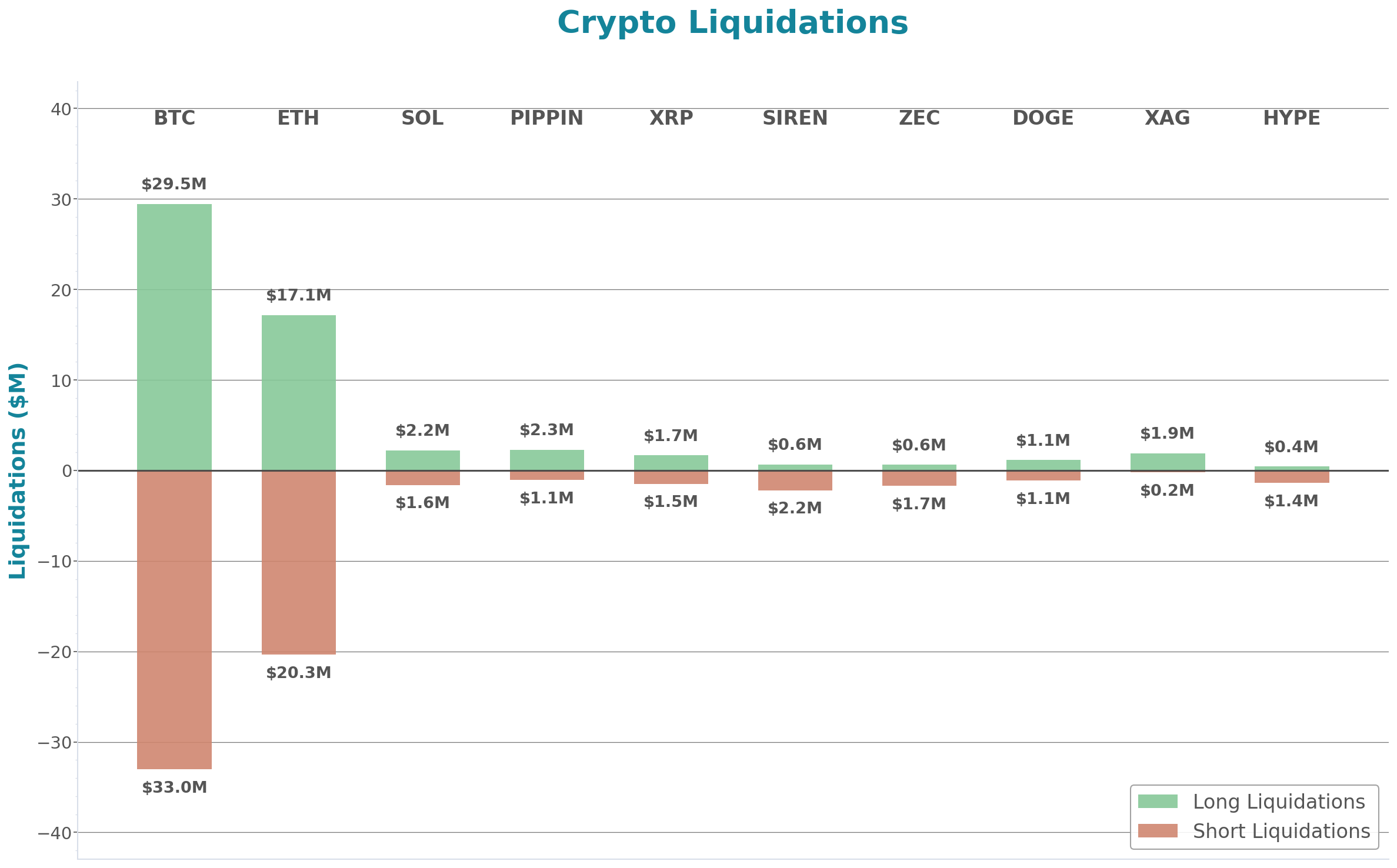

Bitcoin inflows to exchanges spike as BTC hits $75,000 resistance, with CryptoQuant analysts noting large deposits are associated with increased selling pressure.